Corporate Adoption For Google Pay Creates Change Champions

A Graduate Capstone Project for University of Massachusetts Project Management MBA Program

Create a Problem Statement: How can Google Pay speed user adoption in the more resistant U.S. market so that the company can overcome competitive obstacles and fuel their global digital banking strategy?

Global cashless payments are slated to increase 80 percent from 2020-2025 and to almost triple by 2030.* The open banking movement is now unfolding with API interface regulations varying country to country. India and UK markets offers key learnings. Along with the digital transformation in how we manage our money in our personal lives, much the same will happen at work. The user experience for those who travel for business will undergo digitalization. Corporate finance, sales, procurement and HR will also feel the shift to open banking. Google Pay is well positioned to be the brand who helps you in every area of your finances. Importantly, with Android users constituting 70% of the global market, Apply Pay will never be able to serve global corporate customers with cross-border, frictionless transactions and cash back rewards like Google can. The North America market growth will lag behind all other global regions, while Asia-Pacific, Africa and Europe market will drive early adoption. By the end of the decade Google Pay will be the device agnostic, bank agnostic global market leader in the digital currency economy, and the preferred choice of merchants and consumers alike for its intelligent, seamless, value-driving benefits.

Google Pay helps users create more money to do more with life.

• Google has ability to work on iphone and android, a large competitive advantage in the early race ahead. Key competitors Apple Pay, Samsung Pay.

• Google offers rewards and cash back, categorizes your spending automatically and links direct to your bank account – all things apply pay is not doing currently.

• Google Pay works thru an API integration with PLAID who retains user data

• Banks will soon offer their own digital wallets. The race is on. Consumer bank loyalty and trust may play a large competitive role, especially among middle income professionals

• Android users more likely to adopt Google Pay, while Apple consumers opting for Apple Pay, unless incentivized to choose GPay

• Google just announced a new security feature of perceived high value. GPay is now able to offer virtual temporary credit card numbers for every transaction, keeping your real credit card number hidden. Game changer.

• Google Pay just announced integration with Alchemy for crypto transactions, enabling crypto in major ways. Game changer.

• Payments tell a bank a lot about consumer behavior – purchase patterns: who, how much and when. Payment transactions generate roughly 90% of banks’ useful customer data. With this data now in the possession of Plaid and Google, risks and issues related to data privacy need to be handled with the utmost scrutiny and caution.

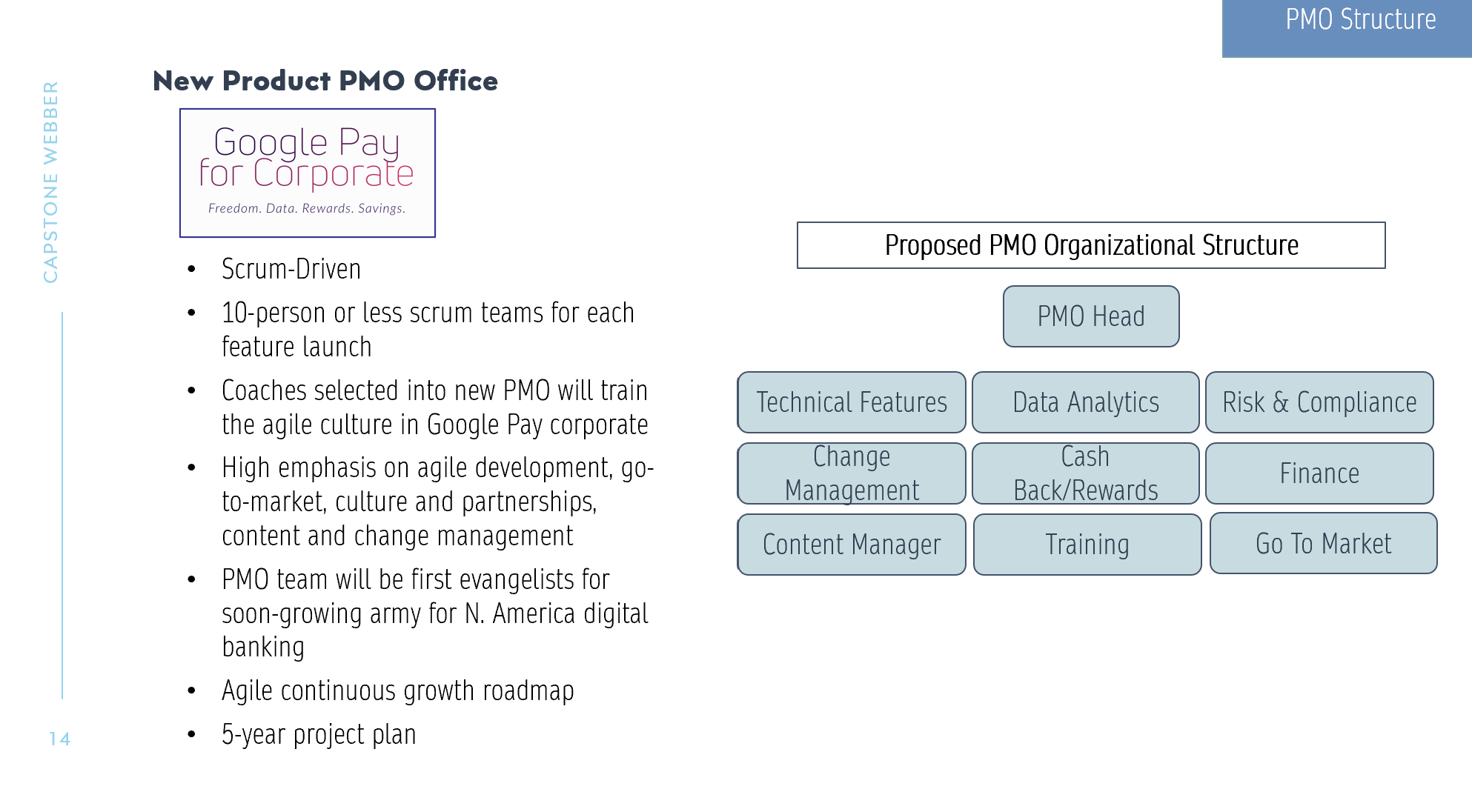

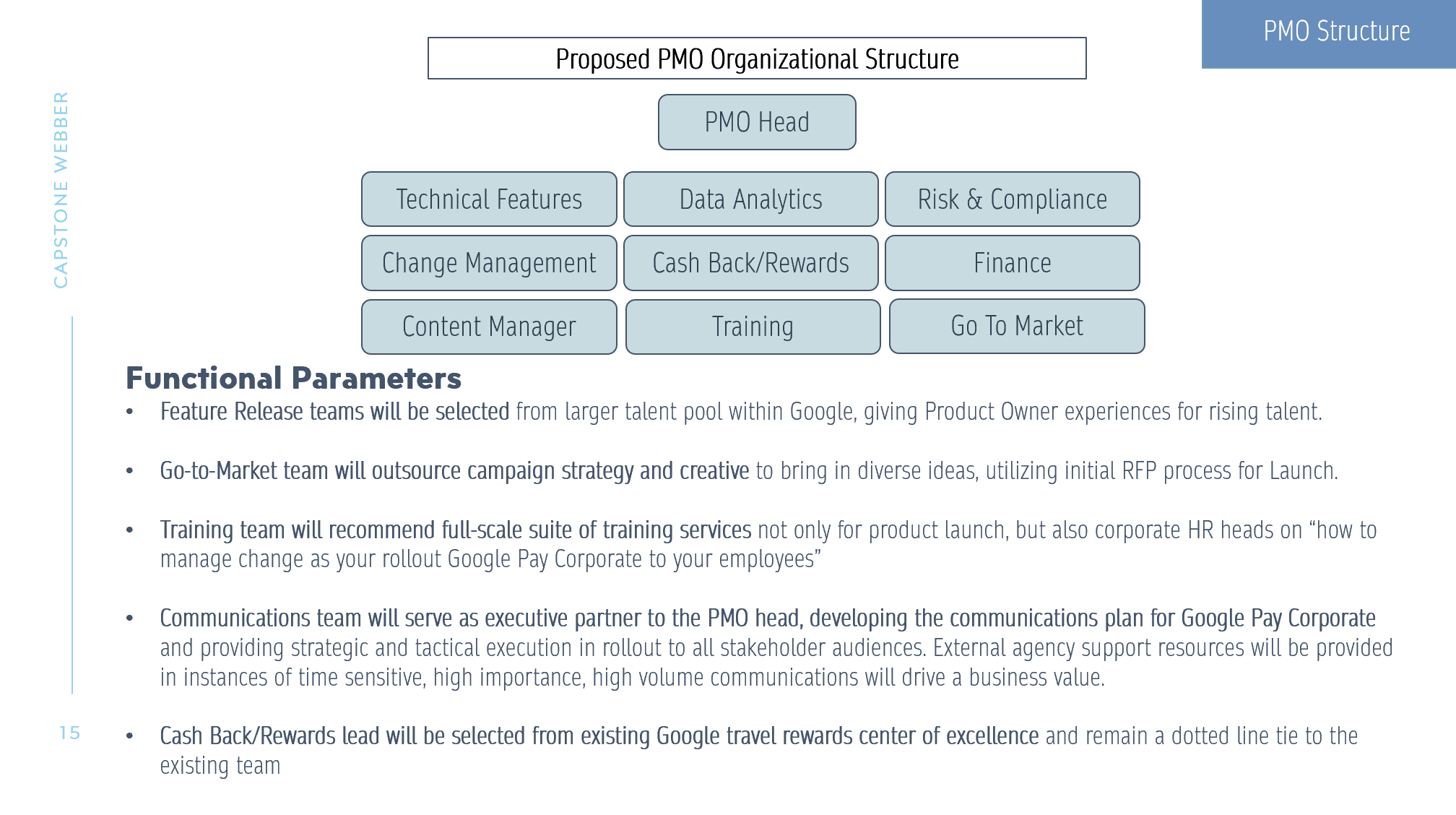

My concept, Google Pay for Corporate, enables North America users to gain exposure to the benefits and ease of use of Google Pay at the office, which will readily translate to personal use. Through the Google Pay for Corporate program strategy, HR Executives win by bringing a solution that will empower, reward and lead employees through digital transformation in key areas like digital finance. The Google Pay for Corporate switch will tightened bonds of global unity through shared experiences and storytelling about digital wallet experiences globally. Done well, it has the power to ignite an employee base of enthusiastic digitalization champions, while also bringing a cost and time saving new UX for corporate expense tracking. HR executives can view Google Pay for corporate as an entry points to open banking that will bring cost savings, time savings and culture-building benefits to the organization.

Imagining an Incremental Roadmap to Key Product Features

Imagine, Sharon, a 38-year-old Boston-based corporate sales executive with frequent global travel for an iconic footwear brand. She needs to save time and avoid expense report hassles. She takes full advantage of airline and credit card cash back offers. She is digitally curious. She is conservative with her personal finances and seeks advice on wealth management, primarily from family and friends and trusted coworkers. She regularly consumes social media for business and personal and is an avid consumer of U.S. pop culture.

With new Google Pay for Corporate, Sharon never needs to create another expense report. She can seamlessly pay for all her travel and business expenses from her Google Pay digital wallet on her watch or phone, android or apple. She’ll be earning cash incentive rewards for business travel she can use any way she likes and Google will spice up the offers with invites and exclusive tickets for America’s most loved events.

Google Pay for Corporate Prototype by Rebecca Webber

Project Charter and Roadmap

Project kickoff workshop can include key leadership from functional teams as the Google Pay for Corporate vision can be a key driver for new cross-functional process consideration in the digital banking landscape. As the group comes together, the program development will enable change impact assessments which will inform future state organization design, while also building the project strategy. Here is my starting point charter and roadmap:

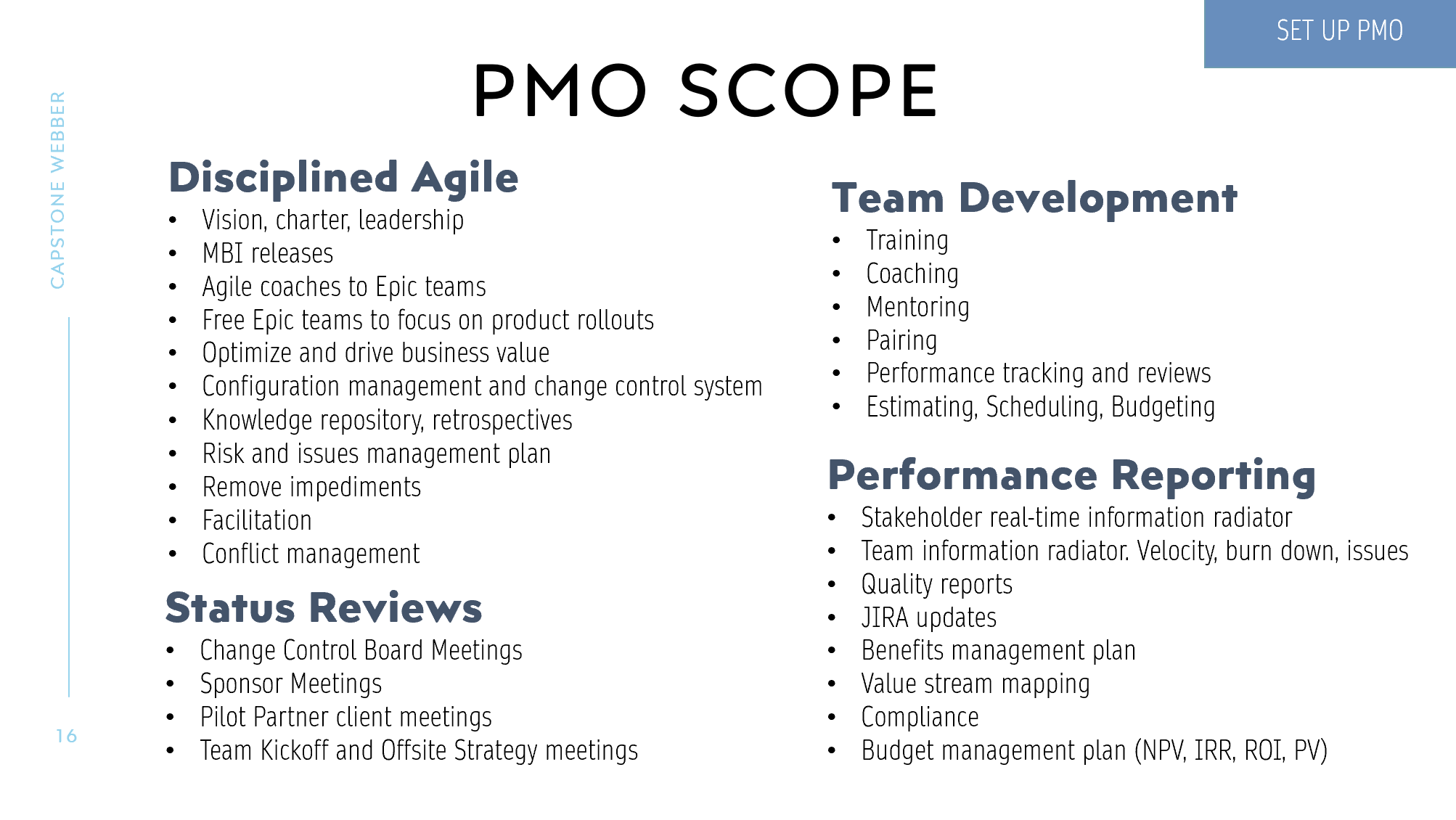

Setting Up A Scaled Agile PMO to Mobilize

With the digital banking landscape unfolding quickly, the Google Pay for Corporate opportunity needs a nimble, integrated team of developers, B2B marketers, finance, HR and legal collaborators on the team.

Stakeholder Engagement Through Strategic Paired Mentoring

In the initial phase, the program team can mobilize support and drive urgency by involving key stakeholders in driving dialogue about the benefits of digital banking. Executives in global regions where digital banking is already well established can speak through existing forums and town halls or through interesting new discussion vehicles. The possibilities for igniting enthusiasm by giving cross-cultural opportunities for organic discussions are endless. We experienced this in a broad and practical sense during the height of the COVID-19 pandemic when scientists joined conference calls from their respective in-country quarantines and described changes in their daily habits and shared how they are managing. The same natural sharing can be true for discussing experiences with digital banking and the coming changes for corporate finance policy changes. Employees (e.g. consumers) must be brought along deliberately and slowly. Through paired sharing of experiences from colleagues they trust from India, UK and Asia, we can enable the change adoption curve.

Insight-Driven Digitalization Change Management for Humans. Now, This is Fun.